Recent months have brought considerable uncertainty to financial markets, driven mainly by the trade policies of U.S. President Donald Trump. The euro has been one of the biggest beneficiaries, strengthening significantly against the U.S. dollar. In early July, the EUR/USD exchange rate reached $1.18, the highest level in four years.* This development has benefited European companies with dollar-denominated costs but could hurt exporters selling in dollars. For investors, it's crucial to understand what’s driving this trend and who stands to gain or lose from it.

Your retention will contact you in a few minutes with more information about this trading strategy.

A Stronger Euro Could Shake Up Stock Markets Too

Confidence in the U.S. Dollar Is Waning

The dollar is under pressure from several directions. The U.S. is facing a deepening budget deficit, compounded by tariffs and a general sense of uncertainty exacerbated by Trump’s administration. According to many experts, this undermines trust in the U.S. currency. Credit rating agency Moody’s even downgraded the U.S. rating from AAA to Aa1. As a result, the market expects the Fed to cut interest rates, likely as soon as September. Two rate cuts are anticipated in total this year. [1]

Lower rates mean reduced yields on U.S. government bonds, diminishing the dollar’s appeal as a safe haven. Meanwhile, the eurozone is recovering from a mild recession. European countries are investing in infrastructure and defense, with Germany approving a massive €500 billion investment fund in March. Although the funds haven’t been fully deployed yet, markets are already reacting positively. The European Commission expects eurozone GDP growth to reach 1.3% in 2025, up from 0.8% in 2024. [2]

Another key factor is yield differentials. While the ECB is also lowering rates, it is doing so cautiously. The market expects at most one more cut this year, after which rates should remain stable. This contrasts with the Fed’s more aggressive stance. As a result, European bonds currently offer more attractive yields than their U.S. counterparts—significantly supporting the euro. ECB President Christine Lagarde emphasized that inflation is now under control and the eurozone has a positive outlook. Foreign investors are increasingly moving capital into Europe.

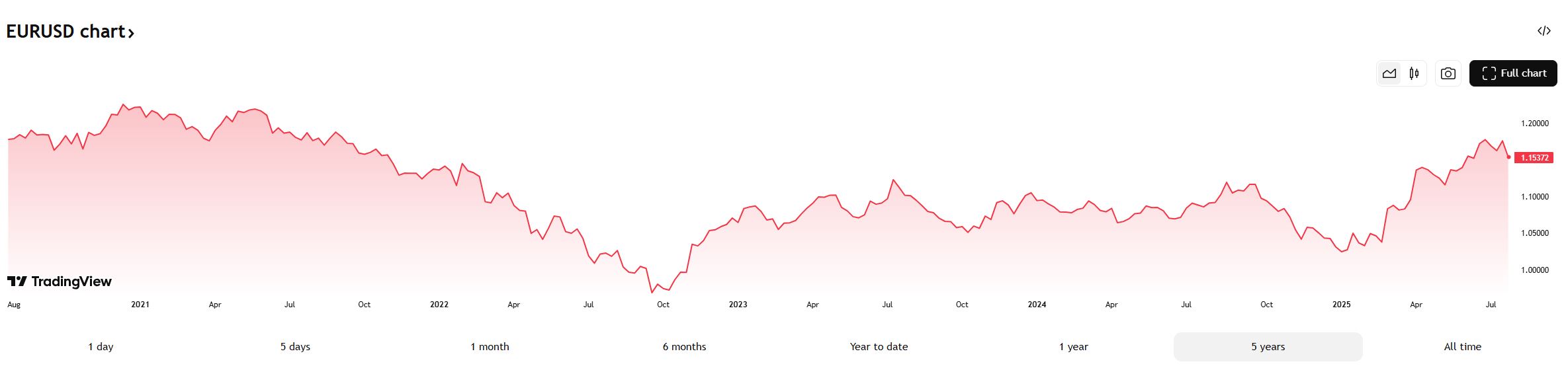

EUR/USD price development over the last 5 years. (Source: tradingview.com)*

Who Profits from a Stronger Euro

Companies with costs in dollars and revenues in euros benefit from a stronger euro. A typical example is airlines such as Lufthansa, Ryanair, and Air France-KLM, which pay for fuel and aircraft leases in dollars. Lufthansa already benefited from lower oil prices in the second half of 2024, and the strong euro is now further boosting its results.

Textile companies like Inditex (owner of the Zara brand) purchase clothing in Asia in dollars. A stronger euro reduces their unit costs, improving margins. Inditex expects that although the exchange rate may reduce revenues by about 3%, cost savings could offset this, making the overall impact positive.

U.S. companies with a large share of revenue from Europe, such as Apple, Microsoft, Coca-Cola, and McDonald’s, report higher dollar income when converting from euros. Apple, for example, generates about a quarter of its revenue from Europe, so a stronger euro can increase its net profit.

Who Suffers from a Strengthening Euro

When dollar revenues are converted into a stronger euro, net profit declines. Airbus, which earns over two-thirds of its revenue in USD, estimates that each one-cent rise in the euro cuts its net profit by 125 million euros. Luxury brands like LVMH and Kering generate 20–30% of their sales in the U.S. A stronger euro makes their products more expensive in the U.S., potentially dampening demand. It also means lower euro-denominated profits when converting from dollars. Dutch company ASML, which produces lithography machines for the semiconductor industry and mainly serves overseas tech firms, also fits this category.

Conclusion

The sudden rise of the euro in the first half of 2025 hit the markets harder than expected. Currency risk remains a key factor for European firms. Investors should monitor how companies hedge against exchange rate fluctuations and whether they can adapt their business models. At the same time, the euro is regaining trust as a currency, which could reshape capital flows in the long term and redirect some investments from the U.S. to European assets. If the euro remains strong in the second half of the year, it will be crucial to watch whether the ECB remains cautious in cutting rates and whether the strong currency starts to overly suppress inflation. This could also influence the direction of eurozone economic policy. [3]

* Past performance is not a guarantee of future results.

[1,2,3] Forward-looking statements are based on assumptions and current expectations, which may be inaccurate, or on the current economic environment, which is subject to change. Such statements are not a guarantee of future performance. They involve risks and other uncertainties that are difficult to predict. Results could differ materially from those expressed or implied in any forward-looking statements.

Disclaimer:

The material herein is considered as marketing communication under the relevant laws and regulations, and as such is not a subject to any prohibition on dealing ahead of the dissemination of investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and should not be construed as containing investment advice, or an investment recommendation, or an offer of or solicitation for any transactions in financial instruments. The published content is intended for educational/informational purposes only. It does not take into account readers’ financial situation, personal experience or investment objectives. APME FX Trading Europe Ltd makes no representation that the information provided is accurate, current or complete; and therefore, assumes no liability for any losses arising from investments based on the supplied content. The past performance is not a guarantee of future results.

Nvidia and AMD shake up the US market with billion-dollar deals

Recent months have brought considerable uncertainty to financial markets, driven mainly by the trade policies of U.S. President Donald Trump. The euro has been one of the biggest beneficiaries, strengthening...

One of Adobe’s Main Competitors Goes Public

Recent months have brought considerable uncertainty to financial markets, driven mainly by the trade policies of U.S. President Donald Trump. The euro has been one of the biggest beneficiaries, strengthening...

AstraZeneca Seeks to Hedge Against Tariffs with an Unprecedented Investment in the US

Recent months have brought considerable uncertainty to financial markets, driven mainly by the trade policies of U.S. President Donald Trump. The euro has been one of the biggest beneficiaries, strengthening...

Risk warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.29% of retail investor' accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Read our Risk Disclosures.